How Drought Affects Real Estate

Drought is the one risk every property depends on — and almost nobody prices in. When it becomes a long-term supply problem, we call it water stress.

- Development halts — in parts of Arizona, new construction stopped for lack of a 100-year water supply

- Service cut-offs — some communities have lost municipal water deliveries outright

- Data center exposure — servers use millions of gallons per day to cool

- Agricultural loss — farm REITs carry direct crop-yield risk

- Utility cost surge — water rates rise sharply as supply tightens

- Demand ceiling — growth stalls where water supply hits a wall

- Lender repricing — mortgage underwriting starting to flag water risk

Location Is Everything

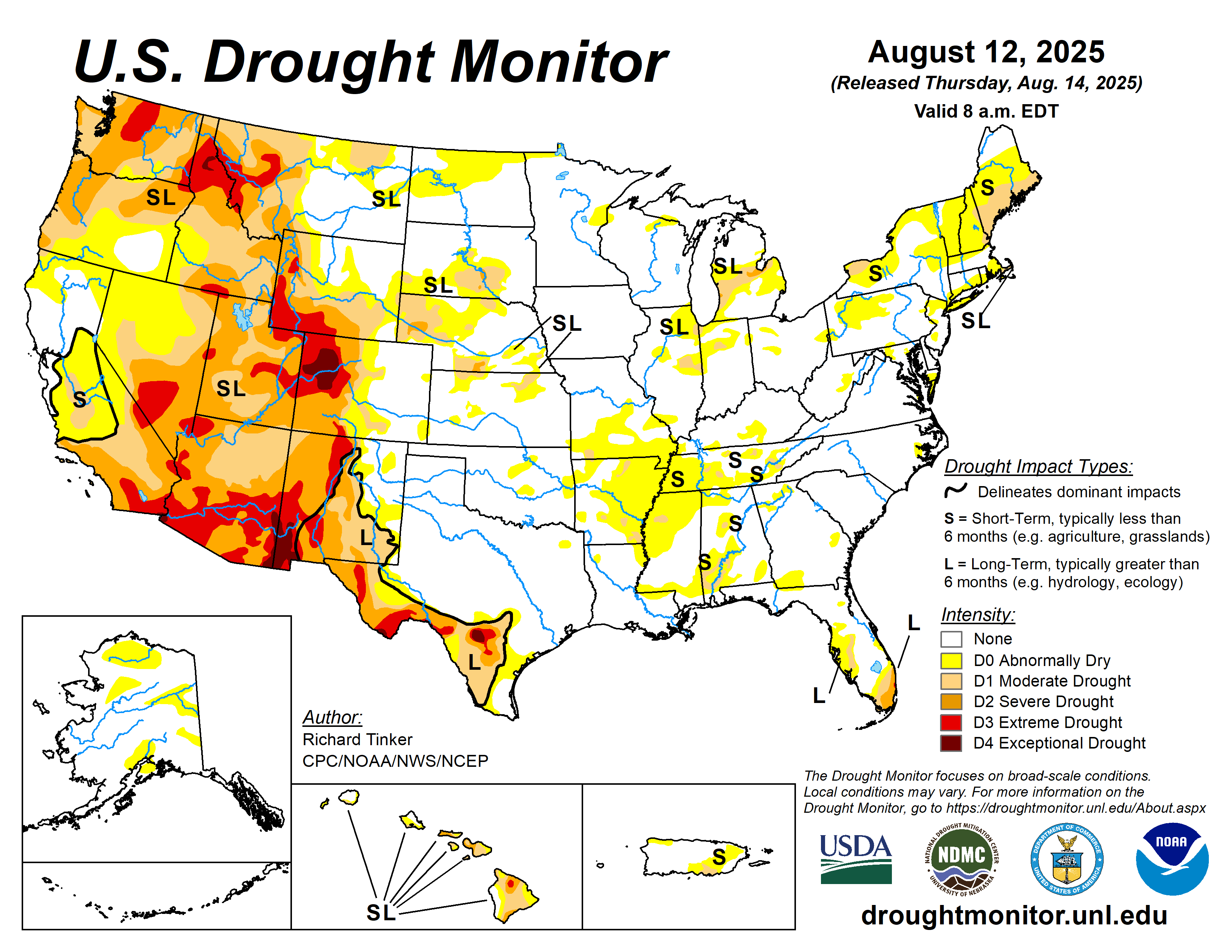

Water stress is uneven across the country. The U.S. Drought Monitor — updated every week by NOAA, USDA, and the National Drought Mitigation Center — shows which parts of the country are in severe or exceptional drought right now. The western U.S. and southern Plains dominate the long-term picture, but drought has been expanding into the Midwest and Southeast.

Two REITs with Sun Belt exposure can have completely different water economics depending on which river basins and aquifers their properties actually depend on.

What Drought Is — and Why It's Different Now

Drought happens when an area gets significantly less rain than normal over an extended period, depleting rivers, reservoirs, and underground water supplies. Short-term drought dries out crops. Long-term drought drains the aquifers that millions of homes and businesses depend on.

What's changed is permanence. The western U.S. has been in a megadrought — a drought lasting 20+ years — since around 2000. Research in Nature Climate Change found it's the driest 22-year period in at least 1,200 years, with roughly half its severity linked to climate change. This isn't a dry spell waiting to end. It's a new baseline.

The Colorado River: A Case Study in Systemic Risk

The bathtub ring at Hoover Dam

Lake Mead looking toward Hoover Dam. The bright white band on the canyon walls — the "bathtub ring" — marks where the water level used to sit, more than 100 feet higher than recent lows. Every foot the lake drops is another round of allocation cuts to Arizona, Nevada, and California.

.jpg){kind=link}

No story illustrates drought's threat to real estate better than the Colorado River. It supplies water to Arizona, Nevada, California, Colorado, Utah, Wyoming, and New Mexico — including Phoenix and Las Vegas, two of the fastest-growing real estate markets in the country.

Lake Mead, the river's largest reservoir, dropped to just 27% of capacity in July 2022 — its lowest level since it was filled in the 1930s. The federal government declared the first-ever water shortage on the river that year, triggering mandatory cuts to Arizona and Nevada's water allocations.

The core problem: water rights on the Colorado were set in 1922, during one of the wettest periods in the river's recorded history. They assumed far more water than the river typically carries — and climate change is reducing that flow further. Seven states and 40 million people are staked on a system built for a climate that no longer exists.

When Water Stops Arriving

In parts of Arizona, new home construction has been halted because developers can't prove a 100-year water supply, as state law requires. In 2023, Rio Verde Foothills — a Phoenix suburb — had its water supply cut off entirely when Scottsdale stopped delivering water it could no longer spare. Hundreds of homeowners were left scrambling.

For REITs, drought exposure cuts across multiple asset classes. Data centers use millions of gallons per day to cool servers. Agricultural REITs are directly exposed to crop failures. Even residential REITs face headwinds when a community stops growing because water supply has hit a ceiling.

Lenders are starting to notice. Fannie Mae research has flagged water availability as an emerging risk in mortgage underwriting. When major lenders start pricing water risk into loan terms, property values in constrained markets will feel it — the same way they felt it after flood risk was repriced post-Katrina.

What the Market Already Knows

Water isn't a named peril on most property policies — but lenders, utilities, and municipal bond buyers are still pricing it. Utility tariffs are rising. Municipal bonds tied to water-supply agencies are getting repriced. The World Resources Institute ranks 25 countries — home to 1.8 billion people — as facing extremely high water stress today. Reinsurers and major asset managers have quietly added chronic water risk to their real estate analytics.

Insurance math, not politics

Water risk shows up in operating costs, development permits, and loan terms long before it shows up in the news. Lenders, utilities, and municipal bond buyers price it because the cuts, the moratoria, and the rate hikes are already landing.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. An apartment REIT concentrated in Phoenix and Las Vegas has a different water-risk profile than one in the Great Lakes region. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A single bad year on the Colorado River doesn't hit one property — it tightens water budgets across every metro that depends on that river system at the same time. That's correlated risk: bets that look different but move together when the reservoirs drop.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio depends on the same shrinking aquifer, or how many REITs in the index share the same river basin.

The CLIMX index is built differently. It uses the same physical-risk models insurers and lenders use — applied building by building across every REIT — and measures how much of a fund's exposure clusters on the same risk. Lenders, utilities, and municipal bond buyers are already repricing water. Most indexes aren't.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use risk models that price drought and water scarcity alongside acute perils — at the property and portfolio level — to build a real estate index with climate risk priced in.