How Heat Stress Affects Real Estate

Heat damage doesn't come in one big event. It compounds — in operating costs, in wear, and in demand.

- HVAC cost surge — cooling bills climbing sharply in the hottest markets

- Equipment wear — chillers, compressors, and rooftop units fail faster

- Roofing breakdown — membranes and shingles degrade under sustained high heat

- Building envelope stress — thermal cycling shortens the life of facades and seals

- Tenant retention — livability and productivity decline in chronically hot markets

- Insurance opacity — heat risk is rarely a named peril on policies

- Migration pressure — demand shifts as markets get less comfortable to live in

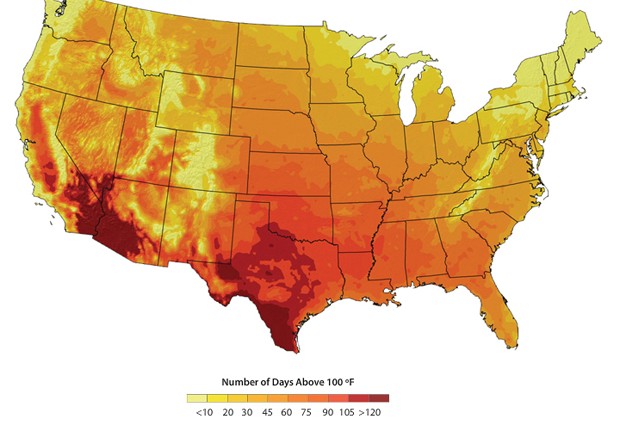

Location Is Everything

Extreme-heat exposure is already uneven and getting more so. This NOAA Climate.gov projection shows expected annual days above 100°F across the U.S. by 2080–2099 under a higher-emissions path. The Sun Belt and Mountain West absorb the biggest increases — but even parts of the East Coast move into Texas-today territory.

Two REITs with apartment or industrial exposure in the Sun Belt can have very different heat economics depending on which metros, which neighborhoods, and which building stock they own.

How Heat Stress Works — and Why It's Getting Worse

Heat stress isn't just uncomfortable summers. It's what happens when the human body can no longer cool itself down. When air temperature combines with humidity, the "feels like" heat index can be 10–20°F higher than the thermometer reads. Above a heat index of 103°F, the body struggles to shed heat even in the shade. Above 124°F, extended exposure can be fatal.

Cities make this worse. Buildings, pavement, and rooftops absorb heat during the day and release it at night — the urban heat island effect. In Phoenix, Miami, and Houston, overnight lows during a heat wave can still exceed 90°F. The body gets no overnight recovery. HVAC systems get no break.

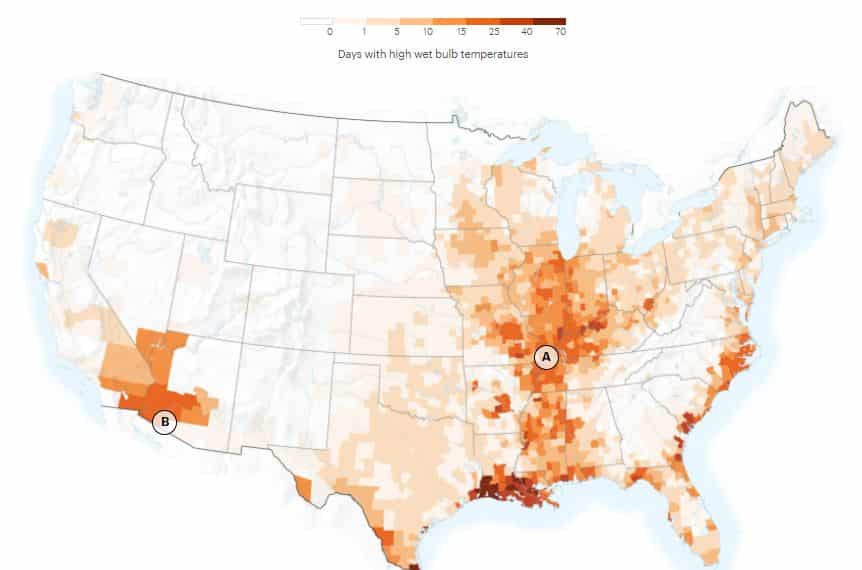

There's a harder physical ceiling called wet-bulb temperature — the lowest temperature a body can reach through sweating. Once the wet bulb passes roughly 35°C (95°F), even a healthy person at rest in the shade with unlimited water cannot shed heat. Outside exposure at that level is as dangerous as a blizzard: exposure kills, and survival depends on getting inside.

Where wet bulb is already dangerous

This map shows where on Earth dangerous wet-bulb temperatures are already occurring or projected to spread. The Persian Gulf, South Asia, and parts of the U.S. Southeast have already brushed the survivability threshold. As these thresholds get crossed more often, affected regions become materially less habitable — and, for real estate, materially less desirable.

Source: Raymond et al., Communications Earth & Environment (2022)

NOAA data shows all ten of the hottest years on record have occurred since 2010. Heat waves that used to happen once every 50 years are now happening roughly once a decade — and that gap is shrinking.

Where Heat Is Redefining Real Estate

The Sun Belt — Phoenix, Las Vegas, Dallas, Houston, Miami — is on the front lines. Phoenix recorded 31 consecutive days above 110°F in the summer of 2023, with overnight lows barely below 90°F. The city recorded 645 heat-associated deaths that year — its deadliest heat season on record.

The Pacific Northwest showed what heat can do to places not built for it. The June 2021 heat dome sent Portland and Seattle — cities designed for cool, mild weather — past 116°F. Nearly 800 deaths were attributed to the event across Washington and Oregon. Buildings without air conditioning became dangerous within hours. Scientists estimated the event was virtually impossible without climate change.

The Operating Cost Problem

Extreme heat is a chronic risk — it doesn't arrive as one dramatic event but accumulates over years and decades. That makes it easy to miss in a quarterly earnings report. But compounding operating costs, declining livability, shifting migration patterns, and rising insurance premiums are already showing up in the data.

A 2022 study in Communications Earth & Environment by researchers at the University of Washington found that even if warming is limited to the Paris Agreement's 2°C target, exposure to dangerous heat index levels will likely increase 50–100% in the tropics and 3–10 times across the midlatitudes by 2100. For real estate, that's an operating cost curve that keeps bending upward.

What the Market Already Knows

Heat isn't a named peril on most property policies — but lenders, utilities, and insurers are still pricing it. Moody's and MSCI now track chronic heat in their real estate risk tools. Electric utilities in Texas and Arizona price demand charges around peak-heat days. Moody's RMS and other model providers publish multi-decade heat projections that large asset managers already buy. The market is repricing heat quietly, one line item at a time.

Insurance math, not politics

Chronic heat shows up in operating costs, demand, and insurability long before it shows up in the news. Lenders, insurers, and utilities price it on the margin because the claims, the bills, and the move-outs are already landing.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. A Phoenix apartment REIT has a different cooling-cost curve than a Pacific Northwest one. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A record heat summer doesn't hit one apartment — it pushes cooling costs up across every building in every Sun Belt market at the same time. That's correlated risk: bets that look different but move together when the grid is pushed to its limit.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio sits in chronic-heat metros, or how many REITs in the index share the same Sun Belt exposure.

The CLIMX index is built differently. It uses the same physical-risk models insurers and reinsurers use — applied building by building across every REIT — and measures how much of a fund's exposure clusters on the same risk. The market is already repricing chronic heat quietly, one line item at a time. Most indexes aren't.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use the same physical-risk models insurers use to price chronic heat alongside acute perils — at the property and portfolio level — to build a real estate index with climate risk priced in.