How Hail Affects Real Estate

A single storm can damage thousands of buildings at once. Insurers call it a "shock loss." Hail is usually grouped with tornadoes and damaging straight-line winds under the industry term severe convective storm (SCS) — a category that now drives the largest share of U.S. insured losses in most years.

- Roof damage — the single biggest driver of hail claims on commercial and residential property

- Window and facade loss — baseball-sized hail shatters glass and siding

- Fleet damage — parking lots can total hundreds of cars in one afternoon

- Shock-loss events — one storm, one city, hundreds of thousands of claims

- Percentage deductibles — 1–2% of the insured value, per event, in Hail Alley

- Non-renewal on older roofs — insurers use aerial imagery to flag and drop policies

- Operating cost surprise — hail exposure wasn't priced in when many REITs bought

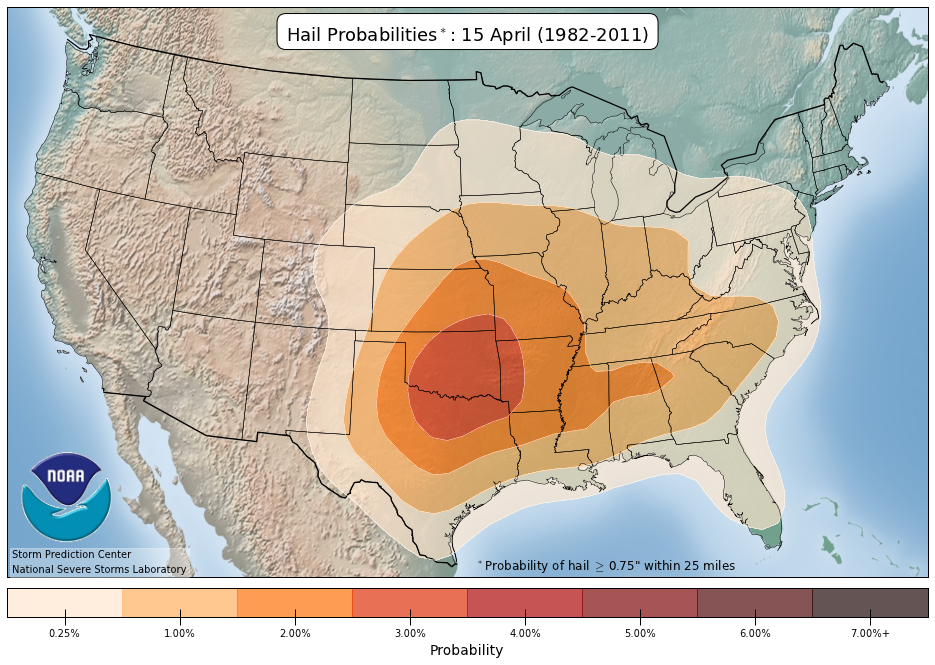

Location Is Everything

Hail risk is regional, not national. This NOAA Storm Prediction Center map shows annual hail density across the United States. The heart of Hail Alley runs through Colorado, Kansas, Nebraska, and Wyoming, with Texas carrying a state-wide hail problem on top. The coasts see far less.

Two warehouses a mile apart can have completely different hail exposure — depending on elevation, roof pitch, and tree coverage. Market-cap indexes can't see that.

How Hail Forms

Hail forms inside powerful thunderstorms. Strong updrafts carry water droplets high into the freezing upper atmosphere, where they turn to ice. Those ice balls get coated in new layers of water on each pass through the storm — growing bigger every cycle — until they're too heavy for the updraft to hold. Then they fall.

Golf ball-sized hail is common. Baseball-sized hail happens more often than you'd think. In extreme cases, hailstones the size of grapefruits — over a pound — have been recorded. When those hit at terminal velocity, they go through roofs, shatter windows, and total thousands of cars at once.

What makes hail so financially devastating isn't just the size — it's the area of impact. A single storm can sweep across an entire city in under an hour, damaging hundreds of thousands of structures simultaneously.

Where Hail Is Redefining Real Estate

The Denver metro has absorbed multiple billion-dollar hailstorms, including a 2017 storm that caused $2.4 billion in damage across the metro in a single afternoon. Texas is a state-wide problem. The DFW metroplex has been hit by multiple billion-dollar hailstorms, and a 2016 outbreak across North Texas caused an estimated $1.5–2 billion in total losses.

In 2023, the U.S. recorded its highest-ever annual losses from severe convective storms — the category that includes hail, tornadoes, and straight-line winds — with multiple individual events each exceeding $1 billion on their own.

Hail has become one of the fastest-growing problems in the U.S. insurance market. Insurers in Colorado, Texas, and Kansas have responded by raising premiums sharply, introducing hail-specific deductibles — often 1–2% of the home's insured value per event — or refusing to write new policies in the most exposed zip codes.

The Roof Problem

Roofs pay first

Aerial view of a single San Antonio home after a hailstorm — every light patch is a damaged shingle, and every damaged shingle is a potential insurance claim. After a bad storm, insurers fly drones over entire neighborhoods and flag homes like this one for non-renewal.

Roofs are the central issue. Insurers now use aerial imagery and machine-learning tools to assess roof condition across entire cities after a storm. Properties with older roofs — common in value-focused REIT portfolios — are increasingly being flagged for non-renewal.

CoreLogic estimates tens of millions of U.S. properties face damaging hail exposure each year. For a $500,000 house, a 2% hail deductible means $10,000 out of pocket before insurance pays anything. For a REIT with thousands of roofs across Dallas, Denver, or Kansas City, those deductibles add up fast.

What Insurers Already Know

The insurance industry has been tracking hail losses more carefully than almost any other peril, because the losses land fast and hard. Insurance Information Institute data puts average annual U.S. insured losses from hail-driven severe weather above $12 billion — one of the costliest natural perils in the country. Munich Re's European data shows the same upward trend across Germany, Austria, and northern Italy.

Insurance math, not politics

Insurers price hail risk based on expected losses from catastrophe models, not beliefs about climate policy. When premiums spike or coverage disappears, it's a balance-sheet decision. The claims data is clear: hail losses are growing, and much of the exposure sits in portfolios nobody has stress-tested.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. Two warehouses a mile apart can have totally different hail exposure depending on elevation, roof pitch, construction materials, and tree coverage. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A single bad storm season in Hail Alley can damage dozens of buildings in the same REIT, or many REITs in the same index, at once. That's correlated risk: bets that look different but move together when the storm cells fire.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio sits under the same supercells, or how many REITs in the index share the same Hail Alley exposure.

The CLIMX index is built differently. It uses the same catastrophe models insurers use — applied building by building across every REIT — and measures how much of a fund's exposure clusters on the same risk. Insurance companies have been pricing hail by the address for years. Market-cap indexes haven't caught up.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use the same catastrophe models insurers use to price hail and severe convective storm risk — at the property and portfolio level — to build a real estate index with climate risk priced in.