How Sea Level Rise Affects Real Estate

Rising water doesn't need a storm to cause damage. The starting point is simply higher every year.

- Sunny-day flooding — high tides regularly flood streets, garages, and basements

- Storm surge amplification — hurricanes reach farther inland because sea level is higher to start

- Saltwater intrusion — corrosion of foundations, rebar, and underground infrastructure

- Insurance withdrawal — the coastal private market is pulling back

- No forward pricing — federal flood insurance (NFIP) isn't allowed to price future sea level

- Price discounts emerging — exposed properties selling below comparable inland homes

- Mitigation spending — seawalls, pump stations, and elevated roads shift onto local taxpayers

- Mortgage-lifetime risk — a 30-year mortgage on a property that may flood within 30 years

Location Is Everything

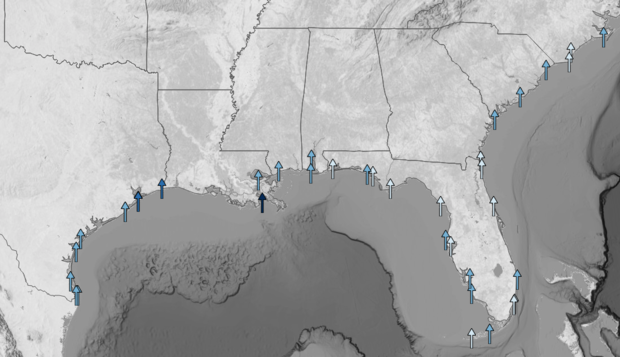

Sea level rise is not uniform. This NOAA tide-gauge map of the Gulf and Southeast Atlantic coasts shows the direction and magnitude of observed sea level trends at each long-term station — most arrows point up, and the Gulf arrows are taller than the Atlantic ones. Within the U.S., the Gulf, Atlantic, and Pacific coasts rise at different rates.

Two REITs with coastal exposure can have very different sea level risk depending on which coast, which county, and which elevation their buildings sit at.

Why Sea Level Is Rising — and Why It Keeps Accelerating

Two things drive sea level rise. First, warmer ocean water takes up more space — an effect called thermal expansion. Second, melting land ice from Greenland, Antarctica, and mountain glaciers flows into the ocean and adds volume. Both have been accelerating.

Global sea level has already risen roughly 8 inches since 1900. The rate of rise is now about 3.7 mm per year and accelerating. NOAA's 2022 Sea Level Rise Technical Report projects an additional 10–12 inches along U.S. coastlines by 2050 — as much rise in 30 years as the country has seen in the previous century.

Where Sea Level Rise Is Redefining Real Estate

The Gulf Coast and Southeast Atlantic see it first. Miami Beach experiences routine "king tide" flooding on sunny days, with water backing up through storm drains into streets, garages, and parking lots — no storm required. Norfolk, Virginia, Charleston, South Carolina, and Savannah, Georgia have all seen sharp increases in high-tide flooding since 2000.

NOAA data shows U.S. Southeast Atlantic and Gulf Coast regions have seen high-tide flooding days rise 400–1,100% since 2000. NOAA projects that by 2050, most coastal regions will experience high-tide flooding between 45 and 85 days per year — up from a few days a year historically.

Sea level rise also amplifies every hurricane that follows. When a storm pushes water inland, it reaches further and flood depths are higher — because the starting point is higher. Homes that have never flooded in a storm are now flooding.

The Pricing Gap

The federal flood insurance program doesn't price projections. It prices the current flood hazard — which means a home that is almost certainly going to flood in the 2040s is still insured today at a rate set for a hazard profile the building faced a decade ago. Private flood insurers are starting to price the forward curve. NFIP isn't allowed to.

Academic research is starting to catch what the maps miss. First Street Foundation and others have documented measurable price discounts on exposed coastal properties — homes in frequent-flood zip codes selling below comparable inland properties. The coastal-premium that once defined U.S. real estate is beginning to erode in the most-exposed markets.

What Insurers Already Know

Reinsurers — the companies that back primary insurers — have been repricing long-horizon coastal risk for years. Catastrophe models from Moody's RMS and Verisk include future climate and sea level rise scenarios as standard inputs. Munich Re and Swiss Re publish annual loss data that shows coastal exposure rising faster than almost any other line of business.

Insurance math, not politics

Reinsurers price sea level rise based on expected future losses from catastrophe models, not beliefs about climate policy. When long-tail coastal coverage gets harder to reinsure, primary insurers pass that cost on to homeowners and commercial property owners. The claims data is clear: coastal losses are growing, and the starting-point water level keeps rising.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. A coastal Florida apartment REIT faces completely different sea level economics than a Rocky Mountain data center REIT. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A slow event — say, a decade of worsening tidal flooding in Miami-Dade — won't hit just one building. It tightens cash flow across every property in the market at the same time. That's correlated risk: bets that look different but move together when the tide keeps creeping higher.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio sits on the same vulnerable coastline, or how many REITs in the index share the same Gulf or Southeast Atlantic exposure.

The CLIMX index is built differently. It uses the same catastrophe models insurers and reinsurers use — applied building by building across every REIT — and includes forward-looking sea level scenarios. Reinsurers have been pricing coastal risk on the forward curve for years. Market-cap indexes haven't caught up.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use the same catastrophe models insurers use to price coastal and sea level risk — at the property and portfolio level — to build a real estate index with climate risk priced in.