How Tornadoes Affect Real Estate

Tornadoes destroy buildings in minutes and reshape insurance markets for years.

- Total loss events — EF4/EF5 tornadoes reduce well-built homes to slabs

- Concentrated damage — a narrow path can destroy hundreds of buildings at once

- No real warning — 15 minutes of lead time at best, versus days for hurricanes

- Deductible shock — percentage-based wind deductibles replace flat deductibles

- Carrier withdrawal — some insurers pulling out of high-risk states entirely

- Rebuild cost surge — materials and labor spike after major outbreaks

- Business interruption — lost rent, lost revenue, displaced tenants

Location Is Everything

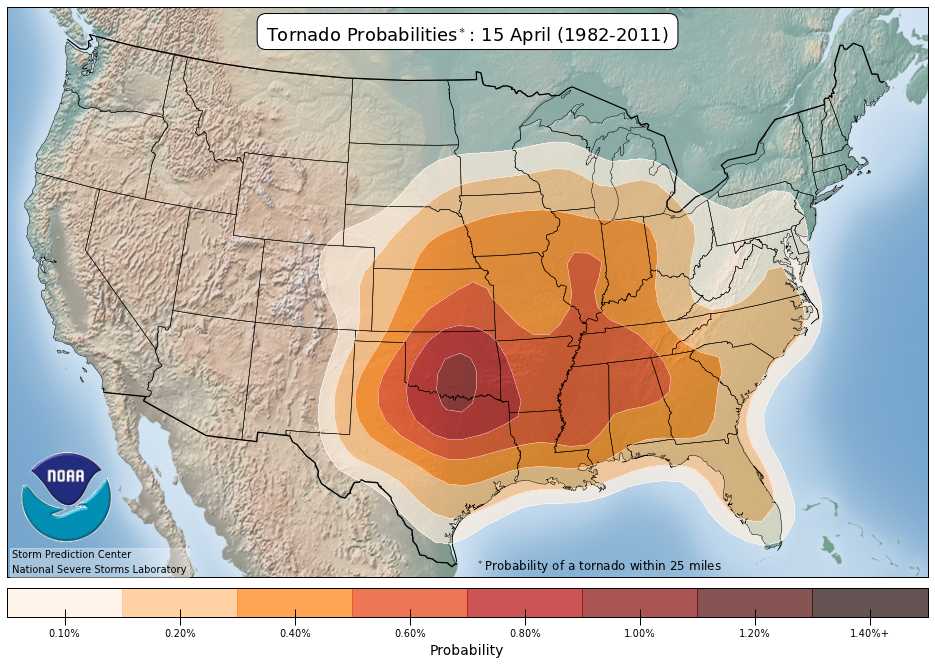

Tornado risk isn't evenly distributed. This NOAA Storm Prediction Center map shows annual tornado density across the United States — the greatest frequency runs from Texas and Oklahoma through Dixie Alley (Mississippi, Alabama, Tennessee, Arkansas), with activity tapering to the West Coast and far Northeast.

Two REITs with industrial or apartment exposure across the South can have wildly different storm profiles depending on which counties they actually sit in.

How Tornadoes Form

A tornado is a violently rotating column of air that reaches from a thunderstorm down to the ground. They form when warm, moist air near the surface collides with cold, dry air above. That clash creates instability — warm air rockets upward, the storm starts spinning, and under the right conditions a funnel drops.

The most powerful tornadoes are rated EF4 or EF5 on the Enhanced Fujita Scale. EF4 winds run from 166 to 200 mph. EF5 exceeds 200 mph. At those speeds, well-built homes don't survive. Cars become projectiles. Entire subdivisions are reduced to concrete slabs.

The U.S. averages more than 1,200 tornadoes per year — more than any other country. That's partly geography: nowhere else has the same collision of Gulf moisture, Rocky Mountain dryness, and cold Arctic air pushing south across flat land.

Where Tornadoes Are Redefining Real Estate

Most people picture Tornado Alley — Texas, Oklahoma, Kansas, and Nebraska. The 2013 Moore, Oklahoma EF5 tornado was nearly a mile wide, killing 24 people and causing $2 billion in damage in just 40 minutes. The April 2011 Super Outbreak produced 360 tornadoes over four days — the largest outbreak ever recorded — killing 321 people and causing around $11 billion in losses.

But the story has shifted. Dixie Alley — Mississippi, Alabama, Tennessee, and Arkansas — is now more active and in some ways more dangerous. Tornadoes here often strike at night, in hilly terrain that limits radar coverage, in communities with older homes and fewer safe rooms. The December 2021 outbreak killed over 80 people across Kentucky and neighboring states — one of the worst December tornado events on record.

What's consistent everywhere: insured losses from tornadoes have grown sharply in recent decades, driven by more development in exposed areas and a documented shift in where and when storms occur.

The Frequency Problem

Scientists debate whether climate change is increasing the total number of tornadoes, but evidence is strong that it's changing where and when they happen. Research published in npj Climate and Atmospheric Science shows tornado activity has shifted eastward — away from the Great Plains and into more densely populated areas. The season is also becoming less predictable, with major outbreaks in months that historically saw little activity.

More people in the path. Less warning. Higher rebuild costs. That's the compound risk that real estate investors need to account for — and that most REIT indexes don't.

What Insurers Already Know

Unlike hurricanes, which give days of warning, tornadoes are nearly impossible to predict more than 15–20 minutes out. That makes rebuilding — not preparation — the insurance industry's primary cost. Rising labor and materials prices have pushed claims well above what insurers collected when policies were written. Several carriers have raised wind deductibles, introduced percentage-based deductibles, or pulled out of high-risk states entirely.

Insurance math, not politics

Insurers price tornado risk based on expected losses from catastrophe models, not beliefs about climate policy. When premiums spike or coverage disappears, it's a balance-sheet decision. The claims data is clear: more development in the tornado path means more expensive losses.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. Industrial parks, apartment complexes, and retail centers across the South and Central U.S. carry tornado risk that doesn't show up in standard financial analysis. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A single outbreak can hit dozens of buildings in the same REIT, or many REITs in the same index, all in one night. That's correlated risk: bets that look different but move together when the sirens go off.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio sits in Dixie Alley, or how many REITs in the index share the same regional exposure.

The CLIMX index is built differently. It uses the same catastrophe models insurers use — applied building by building across every REIT — and measures how much of a fund's exposure clusters on the same risk. Insurance companies have been pricing tornado and wind risk by the address for years. Market-cap indexes haven't caught up.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use the same catastrophe models insurers use to price tornado and wind risk — at the property and portfolio level — to build a real estate index with climate risk priced in.