How Wind Affects Real Estate

Straight-line wind doesn't rotate like a tornado or gather like a hurricane. It arrives as a wall — and it can flatten hundreds of miles of buildings at once.

- Envelope failure — roofs, windows, and cladding take the brunt of the damage

- Downed power — days to weeks without electricity after a major event

- Business interruption — lost rent and tenant displacement during outages

- Tree-strike damage — uprooted trees compound structural loss

- Wind-specific deductibles — insurers separate wind from other perils, often at 1–5% of insured value

- Rebuild cost surge — materials and labor spike after a regional event

- Industrial exposure — warehouses and big-box retail are especially vulnerable to wind loads

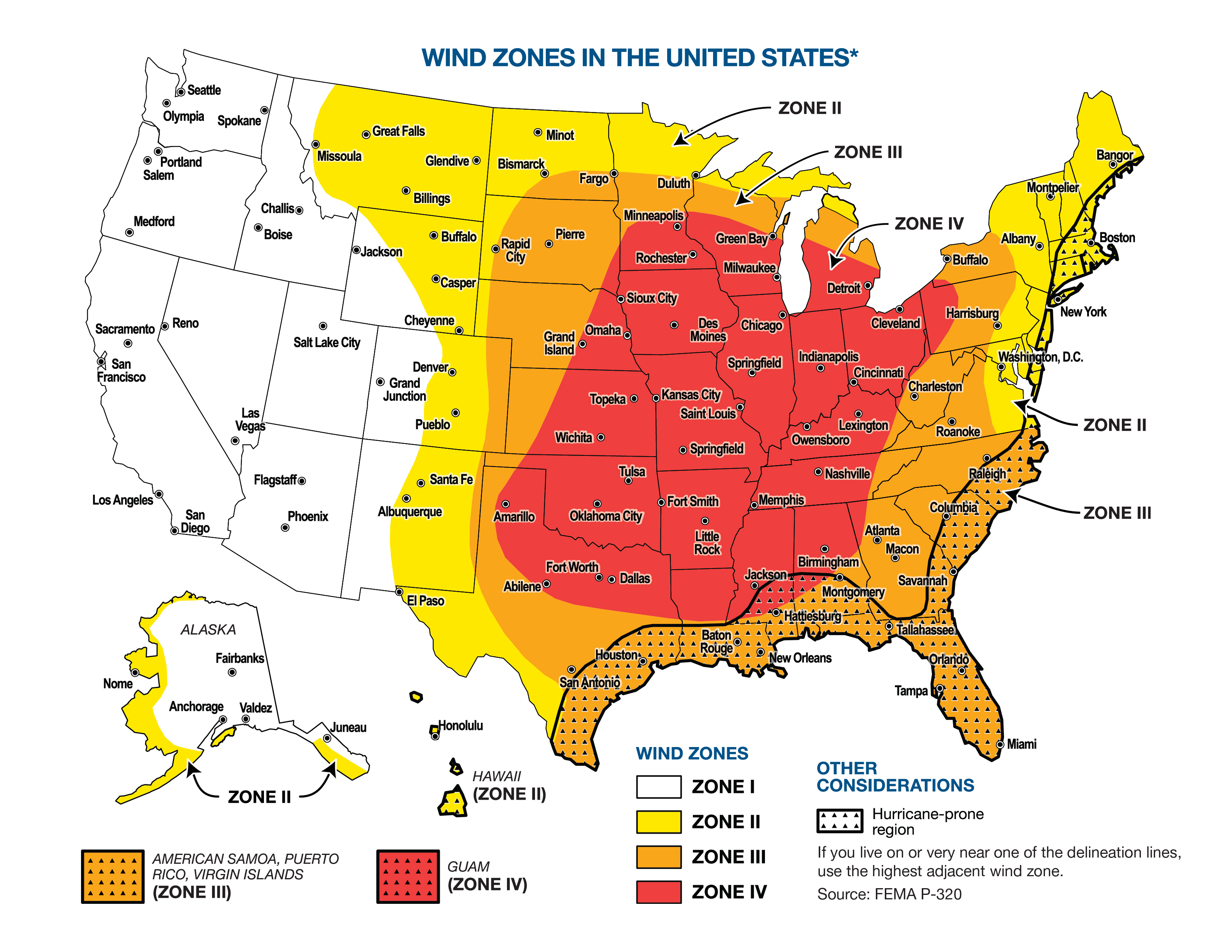

Location Is Everything

Damaging wind affects almost every part of the country, but it doesn't hit everywhere the same. This FEMA wind zone map combines historical data from tornadoes, hurricanes, and straight-line wind events into four zones — Zone I covers the West, Zone IV the central tornado corridor. The Gulf and Atlantic coasts sit inside high-wind zones because of hurricanes.

A warehouse REIT with heavy exposure across Oklahoma, Missouri, and Tennessee carries very different wind risk than one concentrated on the West Coast.

How Severe Wind Works

Severe wind comes in several forms. Thunderstorm downbursts drive concentrated gusts straight to the ground in minutes. Mountain waves create high winds along the Front Range. But the most dramatic are derechos — widespread straight-line windstorms that can travel hundreds of miles along a single line of thunderstorms, producing hurricane-force gusts for hours at a stretch.

Unlike hurricanes, derechos give almost no warning and don't look dangerous on the map until they're already moving. Unlike tornadoes, they don't carve a narrow path — they hit everything along the line at once. A single event can take out power to a million homes and strip the envelope off thousands of commercial buildings.

Where Wind Is Redefining Real Estate

The August 2020 Midwest derecho is the defining modern wind event. In 14 hours, it traveled roughly 770 miles from southeastern South Dakota into Ohio, producing wind gusts over 110 mph in Iowa. More than a million homes and businesses lost power. Total damage reached $11 billion — at the time, the costliest thunderstorm event in U.S. history, and the third severe-weather event since 1980 to exceed $10 billion.

But the 2020 derecho isn't an outlier. NOAA's Storm Prediction Center has catalogued derechos in most years of the modern record. 2023 recorded the highest-ever annual losses from severe convective storms in the United States — a category that bundles wind, hail, and tornadoes together because insurers can't cleanly separate them at claim time.

Wind also amplifies every other atmospheric peril. It drives hurricane storm surge. It spreads wildfire. It hurls hail and debris at buildings. Wind is often the reason another peril becomes catastrophic.

The Building Envelope Problem

When the envelope fails

Naval Air Station Pensacola, September 2004. Hurricane Ivan tore the roof off Building 27 — the photo lab. The envelope failed; everything inside was exposed.

{kind=link}

Wind damage is mostly an envelope problem — the roof, the walls, the windows. And envelope quality varies dramatically across the U.S. building stock. A tilt-up concrete warehouse in Texas is designed for very different wind loads than a pre-engineered steel building in Iowa, which is designed for different loads than a wood-framed apartment building in Georgia.

Insurers know this and have responded by separating wind from other perils on most commercial and many residential policies. Wind-specific deductibles — often 1–5% of the insured value per event — are standard across much of the Midwest and South. A single derecho can push every building in a portfolio through its deductible at the same time.

What Insurers Already Know

Insurance Information Institute data shows severe convective storms — the category that includes derechos, thunderstorm winds, hail, and tornadoes — now account for the majority of annual U.S. insured catastrophe losses. Reinsurers have been repricing wind-driven exposure upward for more than a decade. Property-catastrophe models from Moody's RMS and Verisk include wind events at the event-set level, calibrated against decades of claims.

Insurance math, not politics

Insurers price wind risk based on expected losses from catastrophe models, not beliefs about climate policy. When wind deductibles get separated from other perils or pushed up, it's a balance-sheet decision. The claims data is clear: severe convective storms — wind included — are the fastest-growing line item on U.S. property loss accounts.

Why This Matters

REITs — real estate investment trusts — own physical buildings in specific locations. An industrial REIT with warehouses along the Corn Belt has a different wind profile than one on the West Coast. That's the property-level problem: where a building sits shapes what it's worth.

But portfolios have a second problem. A single derecho doesn't hit one warehouse — it can damage dozens of buildings in the same REIT, or many REITs in the same index, in one afternoon. That's correlated risk: bets that look different but move together when the gust front rolls through.

The index underlying VNQ, and most other U.S. real estate funds, weights REITs purely by market capitalization. It doesn't look at how much of a REIT's portfolio sits on the same derecho corridor, or how many REITs in the index share the same regional wind exposure.

The CLIMX index is built differently. It uses the same catastrophe models insurers use — applied building by building across every REIT — and measures how much of a fund's exposure clusters on the same risk. Reinsurers have been repricing wind exposure for over a decade. Market-cap indexes haven't caught up.

The First Real Estate Index Built on Insurance-Grade Climate Models

We use the same catastrophe models insurers use to price severe wind risk — at the property and portfolio level — to build a real estate index with climate risk priced in.